Taking out a loan can feel like a huge step—one that opens doors or ties your hands, depending on how you manage it. Whether you’re thinking about financing a home, covering tuition, or just handling an unexpected expense, the decision isn’t always black and white. Loans can be a smart tool or a costly trap, and figuring out which one it’ll be for you depends on timing, terms, and your financial habits. Let’s break down the good, the bad, and everything in between to help you decide if borrowing is the right move.

Why Taking a Loan Can Actually Be a Good Idea

Loans aren’t just about debt—they’re about access. They can give you the breathing room to buy a home, build a business, go back to school, or handle a large purchase without draining your savings. Used wisely, they create space to grow. Borrowing doesn’t always mean you’re struggling; sometimes, it’s a sign you’re planning ahead, taking control, and using leverage smartly.

Keep Your Cash Where You Need It

When you borrow, you don’t have to empty your savings to cover big costs. That means your emergency fund stays intact, your investments stay untouched, and you’ve got a financial cushion if something unexpected happens. Liquidity gives you peace of mind, and a loan lets you keep that peace while still moving forward.

Build Credit While Borrowing

Repaying a loan on time boosts your credit profile. That helps you qualify for better interest rates down the road, whether it’s for a car, a mortgage, or even a business loan. A healthy credit score means you’ve got options—and better deals.

Use Borrowed Money to Create Value

Some loans are investments in your future. Starting a company, renovating a property, or getting a degree can all pay off down the line. If the return outweighs the interest, then that loan becomes a stepping stone, not a setback.

- Mortgages often offer lower interest rates and potential tax advantages.

- Student loans come with delayed payments and usually lower rates.

- Business loans can fund growth, hire talent, or expand operations.

When the money you borrow is used wisely, it can help you build a stronger, more stable financial future.

The Downsides You Can’t Ignore

Borrowing always comes with strings attached. If you don’t plan carefully, those strings can turn into chains. Loans need to be repaid—every single month—no matter what. If your income dips or life throws a curveball, that monthly payment doesn’t go away. And when interest adds up, the final cost can be a lot more than you expected.

Monthly Payments Limit Your Freedom

Once you’ve signed the loan papers, you’ve committed to monthly payments for years. That means less flexibility in your budget and more pressure if your financial situation changes. A job loss or emergency expense can turn manageable debt into serious stress.

Hidden Costs Add Up Fast

Loans are rarely just about the interest rate. Lenders often add fees—processing, insurance, early payoff penalties—that raise the total cost. And if your loan has variable interest, the monthly payment could rise unexpectedly. A €10,000 loan over five years at 12% interest might look simple, but you’ll end up paying well over €13,000 in total when fees are included.

Debt Can Take a Mental Toll

More than half of borrowers report stress linked to their loans. It’s not just about money—it’s about always thinking about what you owe. That can affect sleep, relationships, and long-term well-being. If you’re juggling more than one debt, the pressure multiplies fast.

- High-interest loans, like payday or personal credit lines, grow quickly.

- Defaulting on secured loans could cost you your car or home.

- Debt limits your ability to save, invest, or pivot in a crisis.

Taking on debt without a clear plan can seriously limit your options and hurt more than just your bank balance.

So When Does Taking a Loan Make Sense?

There’s no universal answer—it depends on your reasons and your readiness. If the loan helps you build something that’ll pay off later, and you’ve got stable income and a solid budget, it might be the right call. But if you’re borrowing to cover everyday spending or chasing a lifestyle you can’t afford, it’s probably not the time.

Green Lights for Borrowing

- You’re investing in something that appreciates—like a home or education.

- You’re consolidating high-interest debts into something manageable.

- You have a stable income and a clear repayment strategy.

Red Flags to Watch For

- Your income is unstable or unpredictable.

- You’re borrowing to pay for non-essentials or luxuries.

- Your current debt is already eating up most of your income.

If the loan is filling a short-term hole but creating long-term instability, press pause. It’s better to wait and plan than to rush into a financial commitment you can’t control.

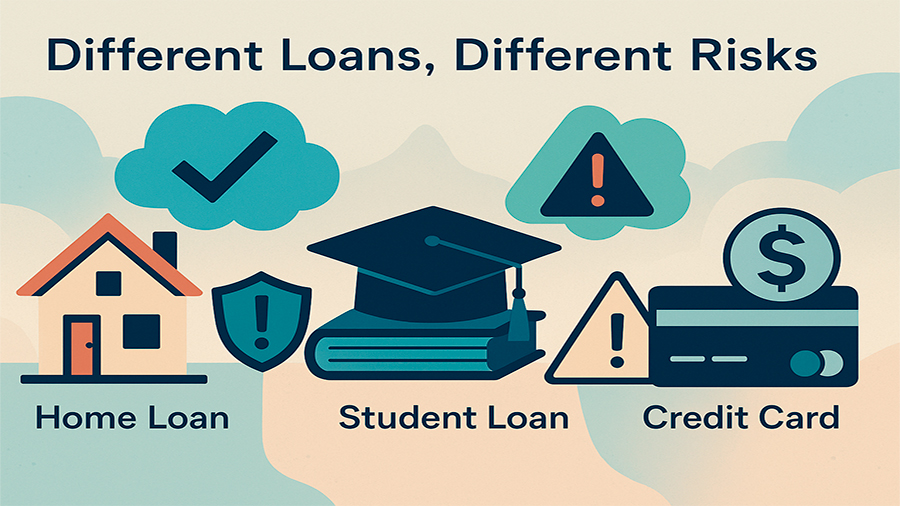

Different Loans, Different Risks

Not all loans are created equal. A home loan, a student loan, and a credit card all work differently. Knowing what kind of loan you’re dealing with—and what risks come with it—helps you make smarter choices. Read everything. Compare lenders. Understand the terms before you commit.

Personal Loans

These are flexible but can get expensive. Interest rates depend on your credit score, and terms range from 1 to 7 years. They’re handy for debt consolidation or one-time needs, but not ideal for ongoing expenses.

Mortgages

These are long-term and usually have the lowest rates, especially if they’re fixed. But they tie you to a monthly payment for decades. Variable-rate mortgages can be risky if interest rates climb.

Student Loans

They’re built for delayed repayment, often starting months after graduation. Public loans usually offer better protections than private ones. But they stick around for years, so make sure your education will pay off.

Credit Lines

Revolving credit is useful in a pinch, but dangerous if you carry a balance. Interest adds up quickly, and it’s easy to spend more than planned. Great for emergencies, bad for big purchases.

Whatever you choose, make sure the loan matches your need—not just your moment.

Know What You’re Signing Up For

Before signing anything, get clear on what it’ll cost you in the long run. The interest rate is just part of the picture. Look at the APR, which includes fees. Check the loan term—longer loans mean smaller payments, but more interest. Watch for things like early payoff penalties or hidden charges that can bite later on.

Things to Compare

- APR: This tells you the full annual cost, not just the rate.

- Monthly payment: Make sure it fits your budget every single month.

- Total cost: What will you pay by the end of the loan, including everything?

Use loan calculators. Read every line of the agreement. Don’t be afraid to ask questions. A lender should be upfront—if they’re not, walk away.

How to Know If It’s the Right Move for You

This part’s personal. Look at your income, your monthly expenses, and your existing debts. Think through your goals. Are you borrowing to fix a problem, or to take a step forward? Could you afford the payments if your income dropped? Do you have a backup plan if things change?

Ask Yourself Before Borrowing

- Do I really need this loan, or just want it?

- Will this create long-term value or just short-term relief?

- Can I repay comfortably, even if something goes wrong?

- Have I compared all my options?

If you can answer “yes” to all of those, you’re probably in a solid position. If not, take a step back. There’s no shame in waiting until the timing—and the numbers—make more sense.

Getting a loan can move you forward, or hold you back. It all depends on how prepared you are, what you’re borrowing for, and how you’ll handle the debt. Use it as a tool, not a lifeline. Borrow with purpose, not panic. And always make sure the loan works for you—not the other way around.